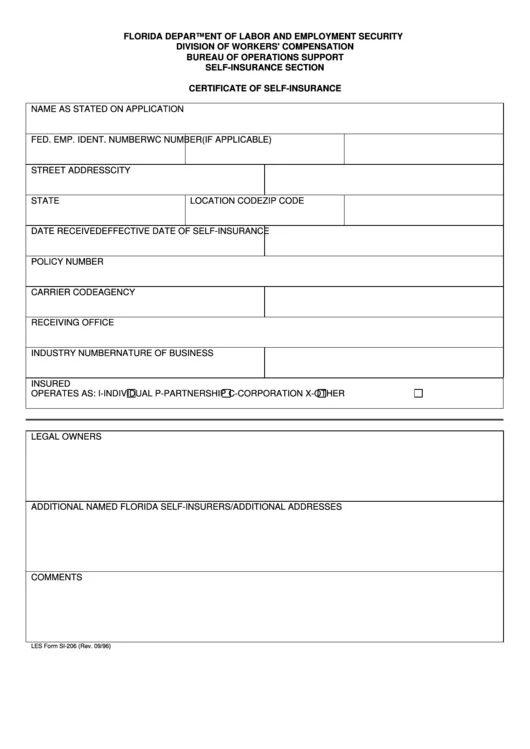

Florida self-insurance certificate requirements for qualified vehicle owners let you legally drive without traditional auto insurance if you meet strict financial responsibility rules. The state allows this for owners who can prove they have the assets to cover accident damages themselves.

As of 2026, Florida requires a surety bond or cash deposit of at least $30,000 for bodily injury or death per person, $60,000 per accident, and $10,000 for property damage. This path isn’t for everyone, but it’s a viable option if you qualify.

Image source: Bing (Web (fair-use with source credit))

Quick Answer

Florida self-insurance certificate requirements for qualified vehicle owners require proof of financial responsibility. You must post a surety bond or cash deposit meeting state minimums. The Florida Department of Highway Safety and Motor Vehicles approves applications.

Qualified owners typically manage large fleets or have significant assets.

What Is a Florida Self-Insurance Certificate and Who Needs One?

A Florida self-insurance certificate is a legal alternative to traditional auto insurance. It proves you can cover accident costs without an insurer. This option is mainly for businesses with large vehicle fleets or individuals with substantial assets.

The Florida Department of Highway Safety and Motor Vehicles oversees the program. It’s not a way to avoid responsibility but a method to self-manage it.

Image source: Bing (Web (fair-use with source credit))

Qualified vehicle owners usually include:

- Companies with 25+ vehicles

- Government agencies

- High-net-worth individuals with multiple high-value vehicles

Why Florida Allows Self-Insurance (And When It Makes Sense)

Florida permits self-insurance to give flexibility to owners who can demonstrate financial stability. It reduces reliance on traditional insurance markets while ensuring accident victims are compensated.

This approach makes sense if you have:

- A large fleet with predictable risk

- Significant liquid assets

- The administrative capacity to handle claims

For most private drivers, traditional insurance remains simpler and more cost-effective. Self-insurance is best suited for organizations with the resources to manage risk internally.

Florida’s Legal Requirements for Self-Insurance

Florida’s self-insurance rules are outlined in Chapter 324 of the Florida Statutes. You must meet the same liability minimums as traditional insurance:

- $30,000 for bodily injury or death per person

- $60,000 for bodily injury or death per accident

- $10,000 for property damage

You’ll need to provide:

- Proof of financial responsibility (bond or cash deposit)

- A completed application to the FLHSMV

- Documentation of your vehicle fleet (if applicable)

The state may also require periodic financial audits to maintain your certificate.

Who Qualifies as a “Qualified Vehicle Owner” in Florida?

Not everyone can self-insure in Florida. The state defines qualified vehicle owners as those who can demonstrate financial responsibility and meet specific criteria.

Typical qualifiers include:

- Businesses with 25 or more vehicles

- Government entities

- Individuals with a net worth exceeding $1 million

The FLHSMV reviews each application individually. Even if you meet the financial thresholds, approval isn’t guaranteed. You’ll need to show you can handle claims and comply with reporting requirements.

How to Apply for a Florida Self-Insurance Certificate

Start by downloading the application from the FLHSMV website. You’ll need to provide your business or personal financial details, vehicle information, and proof of assets.

Submit the completed form with your surety bond or cash deposit. The FLHSMV reviews applications within 30 days. Approval isn’t automatic, so ensure all documents are accurate and complete.

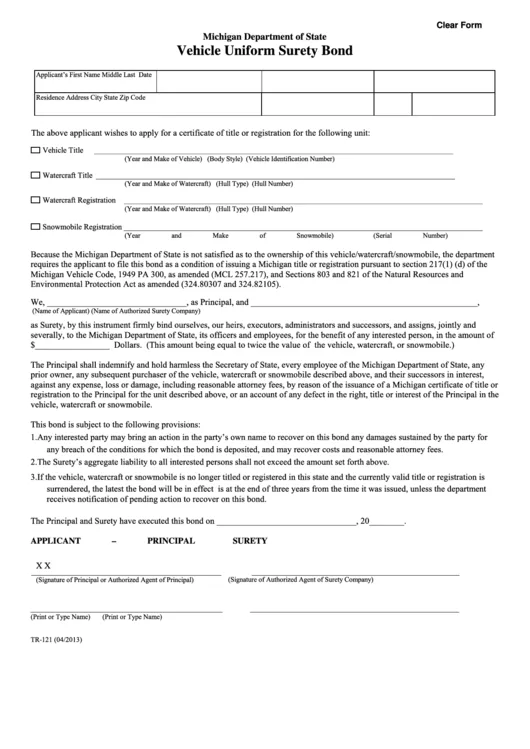

Surety Bond vs. Cash Deposit: Your Two Options

A surety bond is the most common choice. It’s a contract with a bonding company that guarantees payment to the state if you can’t cover accident costs.

A cash deposit is the alternative. You’ll deposit the full required amount with the FLHSMV, which holds it until you no longer need the certificate.

Image source: Bing (Web (fair-use with source credit))

Which is better?

Surety bonds are easier to obtain and don’t tie up your cash. Cash deposits are simpler but require significant upfront capital.

What Happens After You’re Approved?

Once approved, you’ll receive your certificate. You must carry it in every vehicle as proof of financial responsibility.

The FLHSMV may conduct random audits. You’ll need to maintain your financial standing and report any major changes. Failure to comply can result in certificate suspension.

The Risks and Downsides of Self-Insuring in Florida

Self-insurance means you’re on the hook for all accident costs. If a claim exceeds your bond or deposit, you’ll pay the difference out of pocket.

You also take on administrative burdens. Handling claims, paperwork, and reporting can be time-consuming. Traditional insurance shifts these tasks to the insurer.

Common Mistakes That Get Applications Rejected

Incomplete applications are the top reason for rejection. Double-check that all fields are filled and documents are attached.

Underestimating financial requirements is another pitfall. Ensure your bond or deposit meets Florida’s minimums. Misrepresenting assets or vehicle counts will also lead to denial.

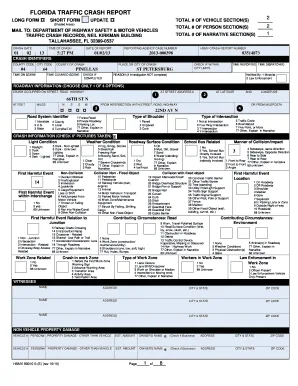

What to Do If You’re in an Accident While Self-Insured

Report the accident to the FLHSMV immediately. You must file a crash report if there are injuries, deaths, or property damage over $500.

Provide your self-insurance certificate to law enforcement and other involved parties. You’re responsible for covering damages directly.

Image source: Bing (Web (fair-use with source credit))

What if the other driver is at fault?

You can still seek compensation from their insurer. But you must prove their liability. Your self-insurance status doesn’t affect their obligation to pay.

Costs: Self-Insurance vs. Traditional Insurance in Florida

Surety bonds typically cost 1 to 3 percent of the coverage amount annually. A $60,000 bond might run $600 to $1,800 per year.

Traditional insurance premiums vary widely but often cost less for average drivers. Self-insurance becomes cost-effective for large fleets with low accident rates.

Hidden costs to consider

You’ll need to budget for claims processing and legal fees. Administrative overhead can add up quickly. Traditional insurers handle these costs for you.

How to Keep Your Certificate Active (And Avoid Penalties)

Submit annual financial statements to the FLHSMV. They’ll verify you still meet the requirements.

Notify the FLHSMV of any major changes. This includes adding or removing vehicles or significant financial shifts. Failure to report can lead to suspension.

What happens if you let it lapse?

Driving without valid proof of financial responsibility is illegal. You’ll face fines, license suspension, and possible vehicle impoundment. Reinstatement requires paying penalties and reapplying.

When Self-Insurance Isn’t the Right Choice

Small businesses with limited assets should avoid self-insurance. The financial risk is too high if a major accident occurs.

Individuals with poor driving records also face higher risks. Traditional insurance provides more protection and predictability. Self-insurance works best for stable, low-risk operations.

FAQs About Florida Self-Insurance Certificates

How long does it take to get approved?

The FLHSMV typically processes applications within 30 days. Complex cases may take longer. Submit all documents upfront to avoid delays.

Can I self-insure just one vehicle?

No. Florida generally requires self-insurance for all vehicles you own. Exceptions are rare and require special approval.

What happens if I sell a vehicle?

Remove it from your certificate immediately. Notify the FLHSMV to update your records. Keeping inactive vehicles on file can cause compliance issues.

Do I still need a license plate?

Yes. Self-insurance doesn’t replace registration requirements. You must maintain valid plates and tags.

Can I switch back to traditional insurance later?

Yes. Notify the FLHSMV when you obtain a policy. They’ll cancel your self-insurance certificate.

There’s no penalty for switching.