Image source: Bing (Web (fair-use with source credit))

If you’ve had your Florida license suspended for a DUI or serious traffic violation, you’re likely dealing with Florida SR22 and FR44 insurance filing requirements for high risk drivers. These filings prove you carry the state-mandated coverage to get back on the road legally.

Florida requires an SR22 for most high-risk cases, but a DUI triggers the stricter FR44 with higher liability limits. As of 2026, the Florida Department of Highway Safety and Motor Vehicles enforces these rules without exception.

Quick Answer

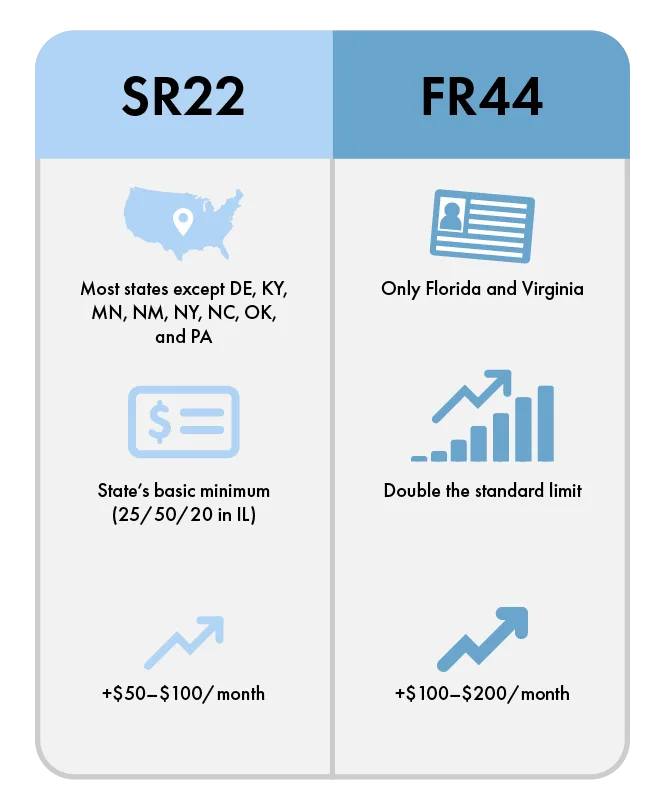

Florida SR22 and FR44 insurance filing requirements for high risk drivers mandate proof of financial responsibility. SR22 requires 10/20/10 liability coverage. FR44 requires 100/300/50 for DUI offenses.

Filings must stay active for 3 years. Lapses trigger automatic license suspension.

What Florida SR22 and FR44 Filings Actually Mean

An SR22 is a certificate your insurer files with the FLHSMV to prove you meet minimum liability coverage. It’s not insurance itself but a guarantee you’re insured. Florida uses it for drivers with serious violations like uninsured accidents or multiple traffic offenses.

An FR44 is Florida’s version for DUI-related offenses. It’s identical in function but demands higher liability limits. Think of it as the SR22’s stricter cousin, reserved for the most serious driving infractions.

When You Need an SR22 vs. an FR44 in Florida

You’ll need an SR22 if your license was suspended for:

- Driving without insurance

- Multiple at-fault accidents

- Excessive traffic violations

- License suspension for non-DUI reasons

You’ll need an FR44 if your suspension stems from:

- A DUI or DWI conviction

- Refusal to submit to a breathalyzer test

- Any alcohol-related driving offense

The FLHSMV determines which filing applies based on your violation. There’s no choice, it’s assigned by the state.

Florida’s Exact Coverage Requirements for SR22 and FR44

Image source: Bing (Web (fair-use with source credit))

SR22 and FR44 filings come with specific liability minimums. These aren’t suggestions, they’re legal requirements.

| Filing Type | Bodily Injury per Person | Bodily Injury per Accident | Property Damage |

|---|---|---|---|

| SR22 | $10,000 | $20,000 | $10,000 |

| FR44 | $100,000 | $300,000 | $50,000 |

Your policy must meet or exceed these limits for the entire filing period. Florida doesn’t accept lower coverage, even if you find a cheaper policy elsewhere.

How the Filing Process Works Step by Step

Image source: Bing (Web (fair-use with source credit))

First, confirm which filing you need by checking your FLHSMV suspension notice. Then, contact an insurer licensed in Florida that offers high-risk filings.

Once you purchase a qualifying policy, your insurer files the SR22 or FR44 electronically with the FLHSMV. This usually takes 24 to 48 hours. You’ll receive a copy of the filing as proof.

Next, pay any required reinstatement fees to the FLHSMV. As of 2026, these range from $150 to $500 depending on your offense. Finally, maintain continuous coverage for the full filing period, typically 3 years.

Costs You’ll Face: Filing Fees, Premiums, and Reinstatement

Expect higher premiums with an SR22 or FR44. Insurers see you as high-risk, so rates often double or triple. The filing fee itself is usually $15 to $50, but the policy cost is where the real expense hits.

FR44 policies are pricier than SR22 because of the higher coverage limits. As of 2026, FR44 premiums in Florida average $200 to $500 per month. Reinstatement fees from the FLHSMV add another $150 to $500, depending on your offense.

Common Mistakes That Get Your License Suspended Again

Letting your policy lapse is the biggest mistake. Even a one-day gap triggers an automatic suspension. The FLHSMV monitors filings in real time, so there’s no grace period.

Switching insurers without confirming the new SR22 or FR44 is filed is another pitfall. Always verify the new policy is active before canceling the old one. Also, don’t assume a standard policy meets the requirements, it must explicitly include the filing.

FR44 vs. SR22: The Key Differences in Florida

Image source: Bing (Web (fair-use with source credit))

The main difference is the trigger. SR22 covers most high-risk violations, while FR44 is strictly for DUI-related offenses. Florida is one of only two states that use the FR44.

Coverage limits set them apart too. SR22 requires 10/20/10, but FR44 demands 100/300/50. That’s why FR44 premiums are so much higher.

Who’s Required to File and for How Long

Florida assigns the filing type based on your violation. If it’s a DUI, you’ll file an FR44. For other serious offenses, it’s an SR22.

The filing period is typically 3 years from the date of your license reinstatement. Repeat offenses or severe violations can extend this. You can’t remove the filing early, even if your driving record improves.

How to Find an Approved Florida Insurer for High-Risk Coverage

Not all insurers offer SR22 or FR44 filings. Start by checking with your current provider. If they don’t, you’ll need to shop around.

Look for insurers licensed in Florida and experienced with high-risk drivers. The FLHSMV website lists approved carriers. Avoid out-of-state insurers, they can’t file with Florida’s system.

What Happens If Your Policy Lapses or You Switch Carriers

A lapse means immediate trouble. The FLHSMV gets an automatic alert if your SR22 or FR44 coverage stops. Your license will be suspended again, and you’ll have to start the filing period over.

Switching carriers is fine, but timing matters. Your new policy must be active and filed before the old one ends. Confirm the new insurer has submitted the SR22 or FR44 to the FLHSMV before canceling the old policy.

Florida-Specific Rules You Can’t Overlook

Florida doesn’t accept out-of-state filings. Your SR22 or FR44 must come from a Florida-licensed insurer. If you move, you’ll need to transfer the filing to a new in-state provider.

Non-owner policies are allowed if you don’t own a vehicle. These still meet the filing requirement but only cover you when driving someone else’s car. The FLHSMV treats them the same as owner policies for reinstatement purposes.

Florida treats SR22 and FR44 filings as continuous obligations. Even if you move out of state, you must maintain the filing until the period ends. The FLHSMV will still monitor your compliance.

If you’re caught driving without the required filing, penalties are severe. You’ll face additional suspensions, fines, and possibly extended filing periods. There’s no leniency for first-time mistakes.

How to Check Your Filing Status with FLHSMV

The easiest way is online. Visit the FLHSMV website and use their driver license check tool. You’ll see if your SR22 or FR44 is active and when it expires.

You can also call or visit a local FLHSMV office. Bring your license and policy details. They’ll confirm your filing status and any outstanding requirements.

Frequently Asked Questions

How long do I need to keep an SR22 or FR44 in Florida?

The standard period is 3 years from your license reinstatement date. Severe or repeat offenses may require longer. The FLHSMV sets the exact duration based on your violation.

Can I get an SR22 or FR44 with a suspended license?

Yes, but you must first satisfy all other reinstatement requirements. This often includes paying fines and completing any court-ordered programs. The filing itself won’t reinstate your license until all conditions are met.

What’s the fastest way to get an SR22 or FR44 filed?

Contact an insurer that specializes in high-risk coverage. Many can file electronically within 24 hours. Avoid providers that require paper filings, as these take longer to process.

Does an SR22 or FR44 cover me in other states?

Your Florida filing meets the state’s requirements, but other states may have their own rules. If you’re driving out of state, check local laws. Some states honor Florida’s filings, while others require their own.

Can I remove an SR22 or FR44 early?

No. The filing period is mandatory. Even if your driving record improves, you must maintain the filing for the full term.

Early removal isn’t an option under Florida law.