Florida penalties for driving without mandatory PIP and PDL insurance can hit your wallet hard and leave you without a license. The state requires all drivers to carry at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL) as of 2026. Skip this coverage, and you’re looking at fines, suspensions, and reinstatement fees that quickly add up.

These aren’t just suggestions, they’re the law. Florida’s no-fault system means PIP covers your injuries regardless of who caused the crash, while PDL pays for damage you cause to others’ property. Get caught without them, and the consequences start immediately.

Image source: Bing (Web (fair-use with source credit))

Quick Answer

Florida penalties for driving without mandatory PIP and PDL insurance start with a $150, $500 fine. Your license and registration get suspended until you pay reinstatement fees and show proof of insurance. Repeat offenses bring higher fines, longer suspensions, and even possible jail time.

You’ll also need an FR-44 certificate if convicted of certain violations.

Why Florida’s PIP and PDL Insurance Rules Matter for Drivers

Florida’s no-fault insurance system means your PIP covers your medical bills and lost wages after a crash, no matter who’s at fault. PDL steps in to pay for damage you cause to someone else’s car or property. Without both, you’re breaking the law and risking financial ruin if you’re in an accident.

The state doesn’t just suggest this coverage, it enforces it strictly. Police can verify your insurance electronically during traffic stops, and the Florida DHSMV tracks compliance in real time.

What PIP and PDL Actually Cover in Florida

PIP covers 80% of your medical expenses and 60% of lost wages up to your $10,000 limit, regardless of fault. It also includes a $5,000 death benefit. PDL, on the other hand, pays for damage you cause to another person’s property, like their car or a fence.

Here’s the breakdown:

| Coverage Type | What It Pays For | Minimum Required |

|---|---|---|

| PIP | Your medical bills, lost wages, death benefit | $10,000 |

| PDL | Damage you cause to others’ property | $10,000 |

PIP doesn’t cover vehicle damage or injuries to others, that’s where PDL and optional coverages like Bodily Injury Liability come in.

Florida’s Mandatory Insurance Requirements (The Legal Minimum)

As of 2026, Florida law requires every registered vehicle to have:

- $10,000 in PIP

- $10,000 in PDL

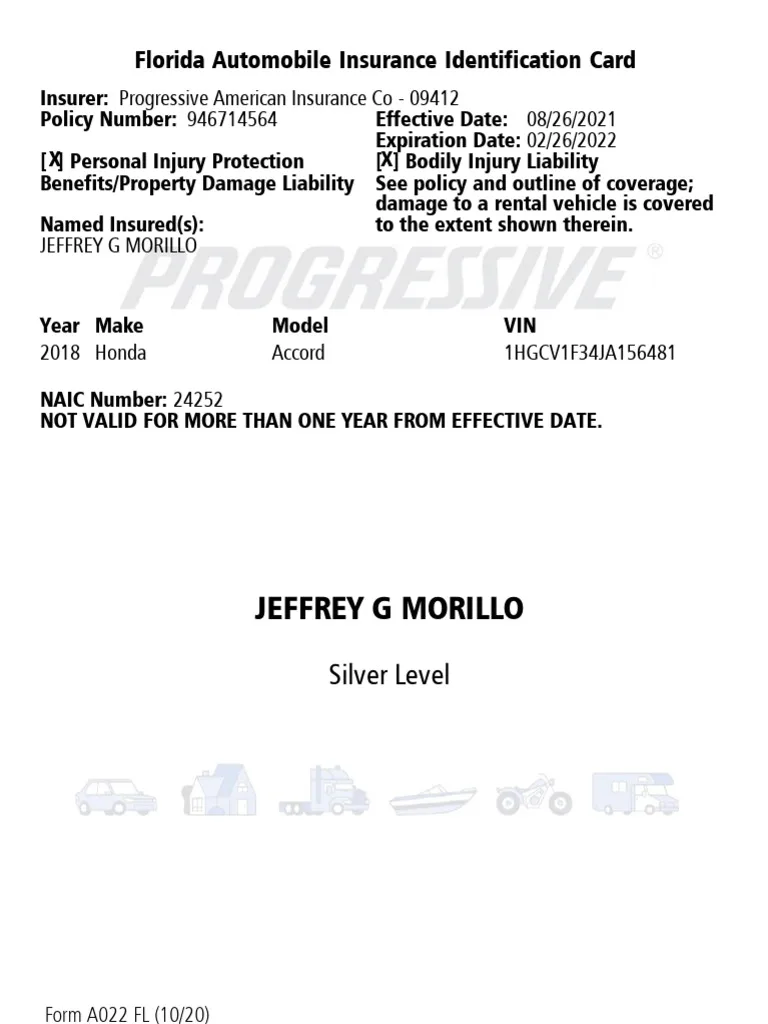

These are the absolute minimums, but many drivers opt for higher limits for better protection. You must carry proof of insurance in your vehicle at all times, either digitally or as a paper copy. The Florida Office of Insurance Regulation oversees these requirements.

If you’re a new resident, you have 30 days to get Florida insurance after registering your vehicle.

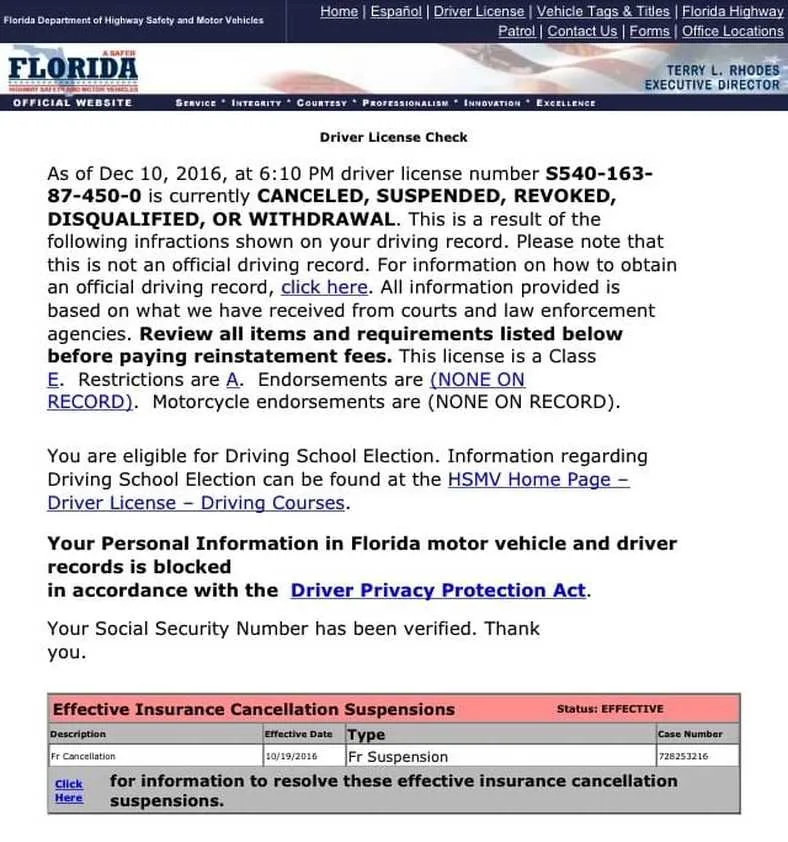

What Happens If You’re Caught Driving Without PIP or PDL?

Get pulled over without valid insurance, and the officer will issue a citation. Your license and registration are suspended immediately unless you can show proof of insurance at the traffic stop.

Image source: Wikimedia Commons / Rusty Clark ~ 100K Photos (CC BY)

The first offense typically results in a fine between $150 and $500. But the real pain comes from the suspension, you can’t legally drive until you reinstate both your license and registration.

Penalties Breakdown: Fines, Suspensions, and Reinstatement Fees

First offense fines range from $150 to $500. Your license and registration are suspended until you provide proof of insurance and pay the reinstatement fee.

The reinstatement fee for a first suspension is $150. For a second offense, the fine jumps to up to $1,000, and the reinstatement fee increases to $250. A third offense can result in a fine up to $5,000 and a $500 reinstatement fee.

Image source: Bing (Web (fair-use with source credit))

If you’re caught driving with a suspended license, you could face additional penalties, including points on your driving record. Four points are added for a first offense of driving without insurance.

How Florida Enforces Insurance Compliance (And How to Avoid Trouble)

Florida uses an electronic verification system to check insurance status during traffic stops. Officers can instantly confirm whether your vehicle is insured. If you’re pulled over and can’t provide proof, you’ll receive a citation.

The Florida DHSMV also conducts random compliance checks. If your insurance lapses, even for a day, the state may suspend your registration.

To stay compliant, always keep your insurance active and carry proof with you. Update the DHSMV if you switch insurers or policies.

Step-by-Step: Fixing a Suspension After a No-Insurance Violation

First, obtain valid insurance that meets Florida’s minimum requirements. You’ll need to provide proof to the court or DHSMV, depending on where your citation was issued.

Next, pay the fine and reinstatement fee. Fees vary based on the offense number, so check your citation or suspension notice for the exact amount.

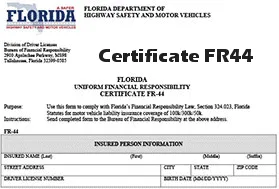

Finally, if required, file an SR-22 or FR-44 certificate. This is a form your insurer files with the state to prove you have the required coverage.

FR-44 vs. SR-22: What Florida Requires for High-Risk Drivers

An SR-22 is a certificate of financial responsibility that proves you have the minimum required insurance. It’s often required after serious violations like driving without insurance or a DUI.

An FR-44 is Florida’s version of the SR-22 but with higher liability limits. You’ll need $100,000 in bodily injury liability per person, $300,000 per accident, and $50,000 in property damage liability. This is typically required after a DUI conviction.

Image source: Bing (Web (fair-use with source credit))

The FR-44 must be maintained for three years from the date of your conviction. If your insurance lapses during this period, your license and registration will be suspended again.

Common Mistakes That Lead to Penalties (And How to Avoid Them)

Letting your insurance lapse, even for a day, can trigger a suspension. Always set up automatic payments or reminders to avoid this.

Driving a borrowed or rented car without confirming it’s insured is another common mistake. If you’re not the primary driver, make sure the vehicle’s insurance covers you.

Not updating the DHSMV when you switch insurers can also cause problems. The state needs to know who your current provider is to verify your coverage.

Cost of Driving Without Insurance vs. Cost of Coverage

The average annual cost for minimum PIP and PDL coverage in Florida is around $1,200 to $1,800. This varies by driver age, location, and driving history.

Compare that to the penalties. A first offense fine of $500 plus a $150 reinstatement fee already matches or exceeds the cost of several months of insurance. Add in potential court costs and increased premiums after a lapse, and the math gets worse.

Driving without insurance also leaves you exposed to lawsuits. If you cause an accident, you’re personally responsible for all damages.

Real-Life Scenarios: What Actually Happens in These Situations?

You get pulled over for speeding and can’t find your insurance card. The officer checks the system and sees your policy lapsed last week. You’ll get a citation, and your license and registration are suspended on the spot.

You’re in a minor fender bender and exchange info with the other driver. They report the accident, and the state discovers you have no insurance. Expect a suspension notice in the mail within days.

You lend your car to a friend who gets into an accident. If your insurance doesn’t cover them, you’re on the hook for all damages.

FAQs About Florida’s PIP and PDL Penalties

What’s the minimum insurance required in Florida?

Florida law requires $10,000 in PIP and $10,000 in PDL. These are the absolute minimums to legally drive and register a vehicle in the state.

How long does a suspension last for no insurance?

Your license and registration stay suspended until you provide proof of insurance and pay the reinstatement fee. There’s no set time limit, it’s up to you to resolve it.

Can I go to jail for driving without insurance in Florida?

Jail time is possible for repeat offenses. A third offense can be charged as a misdemeanor, which carries potential jail time along with higher fines.

What’s the difference between SR-22 and FR-44?

An SR-22 proves you have the minimum required insurance. An FR-44 is Florida’s version for high-risk drivers, requiring higher liability limits. It’s typically needed after a DUI.

How do I reinstate my license after a suspension?

Pay the fine and reinstatement fee, then provide proof of current insurance. If required, your insurer must file an SR-22 or FR-44 with the state.

Does Florida accept digital proof of insurance?

Yes, Florida accepts digital insurance cards on your phone. Just make sure the document is legible and shows all required coverage details.

Final Checklist: Stay Legal and Avoid Penalties

Confirm your policy meets Florida’s $10,000 PIP and $10,000 PDL minimums. Double check the effective dates to ensure there are no lapses.

Carry proof of insurance in your vehicle at all times. Digital or paper copies are both acceptable.

Update the DHSMV if you switch insurers or policies. This ensures the state’s records match your current coverage.

Set up automatic payments or reminders. This prevents accidental lapses that can trigger suspensions.

If you’re a high risk driver, maintain your FR-44 for the full three years. Letting it lapse will result in another suspension.