Florida no-fault insurance law and medical expense coverage means your own car insurance pays your medical bills after an accident, no matter who caused it. This system, called Personal Injury Protection (PIP), is mandatory in Florida and designed to speed up claims while reducing lawsuits.

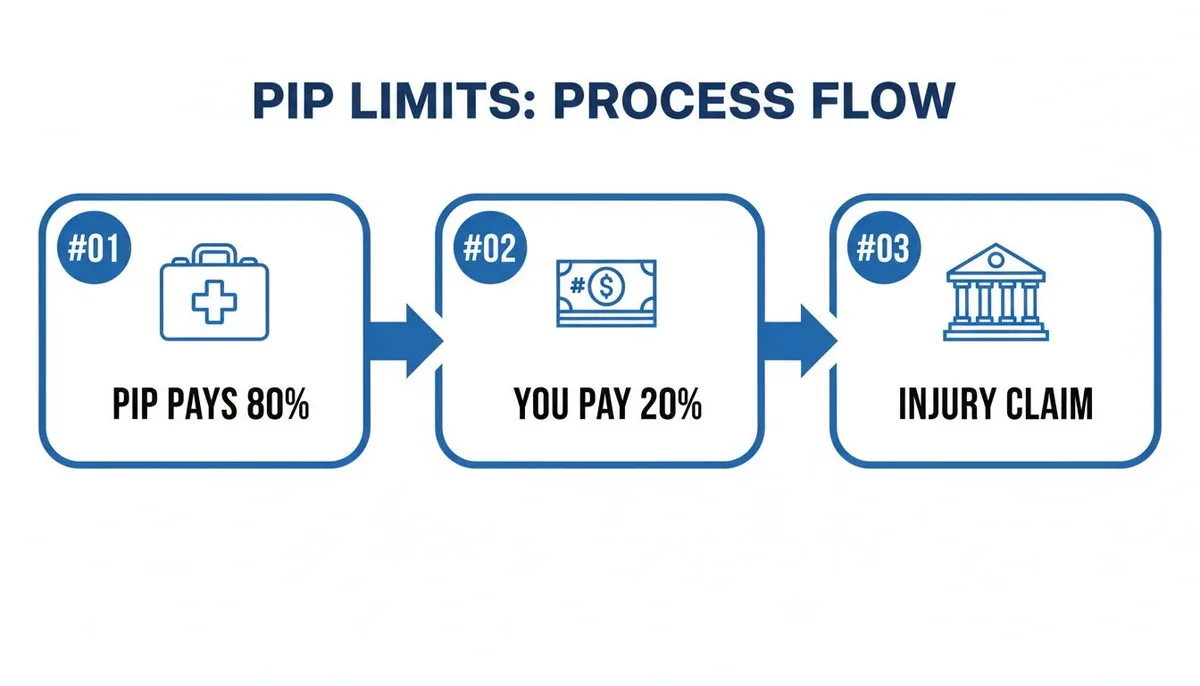

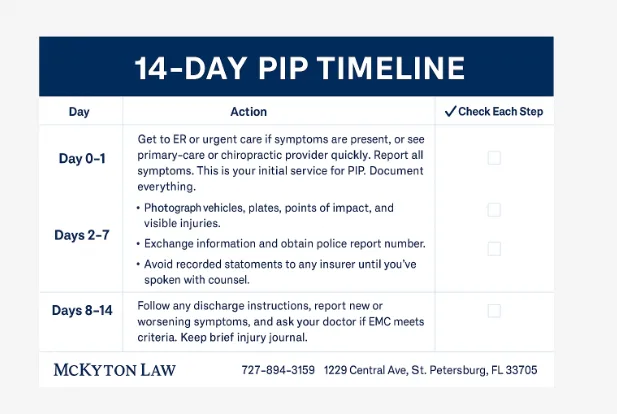

As of 2026, Florida requires drivers to carry at least $10,000 in PIP coverage, which typically covers 80% of medical expenses and 60% of lost wages. But there are strict rules, like the 14-day treatment deadline, that can leave you unprotected if you’re not careful.

Quick Answer

Florida no-fault insurance law and medical expense coverage uses PIP to pay your bills first. Your insurer covers 80% of medical costs up to your policy limit. Lost wages get 60% coverage.

You must seek treatment within 14 days. Missing deadlines can void your claim.

What Florida’s No-Fault Insurance Law Means for Your Medical Bills

Florida’s no-fault system removes the need to prove fault after a crash. Instead, your own insurance, specifically Personal Injury Protection (PIP), kicks in to cover your medical expenses, regardless of who caused the accident.

Image source: Bing (Web (fair-use with source credit))

The trade-off is that you generally can’t sue the other driver unless your injuries meet Florida’s "serious injury" threshold. This includes significant disfigurement, permanent injury, or death. For most minor accidents, PIP is your only recourse for medical bills.

This system aims to reduce court backlogs and get injured drivers treated faster. But it also means you’re limited to your own policy’s coverage, which may not be enough for severe injuries.

How Florida’s PIP Coverage Works After an Accident

PIP is the backbone of Florida’s no-fault insurance law and medical expense coverage. It’s designed to pay out quickly so you can focus on recovery.

Your PIP coverage applies to you, your passengers, and even family members driving your car. It also extends to you as a pedestrian or cyclist if you’re hit by a vehicle. The Florida Office of Insurance Regulation oversees these rules to ensure compliance.

Image source: Bing (Web (fair-use with source credit))

PIP covers three main areas:

- Medical expenses: Up to 80% of reasonable and necessary costs, including hospital stays, surgery, and rehabilitation.

- Lost wages: 60% of your gross income if you can’t work due to accident-related injuries.

- Death benefits: A $5,000 payout to your estate or survivors if the accident is fatal.

Your policy’s limit, typically $10,000, is the maximum PIP will pay, regardless of the actual costs. If your medical bills exceed this, you’ll need other coverage or pay out of pocket.

What Medical Expenses Florida PIP Actually Covers

Not all medical treatments are equal under Florida’s PIP system. The coverage is specific, and some expenses won’t qualify.

Covered medical expenses include:

- Emergency room visits and hospital stays

- Doctor visits, X-rays, and diagnostic tests

- Surgery and physical therapy

- Ambulance services

- Prescription medications

Exclusions are just as important to understand:

- Non-emergency care after the initial treatment (unless classified as an Emergency Medical Condition, or EMC)

- Acupuncture, massage therapy, or chiropractic care (unless referred by a medical doctor)

- Cosmetic procedures unrelated to the accident

- Treatment received more than 14 days after the accident (unless it’s follow-up for an EMC)

The 14-Day Rule and Other PIP Deadlines You Can’t Miss

Florida’s PIP system has strict timelines. Miss them, and you could lose your coverage entirely.

The most critical is the 14-day rule: You must seek medical treatment within 14 days of the accident to qualify for PIP benefits. If you wait longer, your insurer can deny your claim, even if your injuries are severe.

Image source: Bing (Web (fair-use with source credit))

Here’s what else you need to know:

- Initial treatment: Must be provided by a licensed medical doctor, osteopath, dentist, or certain advanced practice nurses. Chiropractors and massage therapists don’t count for the initial visit.

- EMC classification: If your injury is deemed an Emergency Medical Condition, you’re eligible for the full $10,000 in PIP benefits. Without an EMC, your coverage drops to $2,500.

- 60-day payment rule: Your insurer must pay or deny your claim within 60 days of submission. If they miss this deadline, they may owe interest on late payments.

How Much PIP Pays: Limits, Deductibles, and Out-of-Pocket Costs

Florida’s minimum PIP requirement is $10,000, but that doesn’t mean you’ll get the full amount. Several factors can reduce your payout.

First, there’s the deductible. Florida allows PIP deductibles of $250, $500, or $1,000. If you choose a $1,000 deductible, you’ll pay that amount out of pocket before PIP covers the rest.

Lower deductibles mean higher premiums, but less upfront cost after an accident.

Next, co-pays apply to medical expenses. PIP covers 80% of your bills, leaving you responsible for the remaining 20%. For example, if your ER visit costs $5,000, PIP pays $4,000, and you owe $1,000 (plus any deductible).

Here’s a quick breakdown of costs:

| Expense Type | PIP Coverage | Your Responsibility |

|---|---|---|

| Medical bills | 80% | 20% + deductible |

| Lost wages | 60% | 40% |

| Death benefit | $5,000 | None |

Emergency vs. Non-Emergency Injuries: Why the Difference Matters

Florida’s PIP system treats Emergency Medical Conditions differently. An EMC diagnosis unlocks the full $10,000 in coverage. Without it, you’re limited to just $2,500.

A licensed medical professional must classify your injury as an EMC. This includes conditions like severe fractures, head trauma, or internal bleeding. Sprains, whiplash, or minor soft tissue injuries typically don’t qualify.

If your injury isn’t an EMC, you’ll hit the $2,500 cap fast. That’s often barely enough for a single ER visit and follow-up care. Always ask your doctor to document whether your injury meets the EMC standard.

What Florida PIP Doesn’t Cover (And What to Do Instead)

PIP has clear limits. It won’t pay for property damage to your car, that’s what Property Damage Liability (PDL) is for. It also excludes non-medical costs like vehicle towing or rental reimbursement.

Some medical treatments are off the table too. PIP won’t cover acupuncture or massage unless a doctor refers you. Cosmetic procedures, even if accident-related, are also excluded.

For gaps in coverage, consider these alternatives:

- Health insurance: Can cover the remaining 20% of medical bills after PIP pays its share.

- MedPay: Optional coverage that pays medical expenses beyond PIP, regardless of fault.

- Umbrella policy: Extra liability protection if you’re sued for severe injuries.

Step-by-Step: Filing a PIP Claim for Medical Expenses

Start by notifying your insurer immediately after the accident. Even if you feel fine, some injuries take time to appear. Delaying could jeopardize your claim.

Next, seek medical treatment within 14 days. Keep all receipts, medical records, and provider notes. Your insurer will need these to process your claim.

Submit your claim using your insurer’s required forms. Florida uses standardized PIP billing forms that your doctor or hospital must complete. Double-check that all information is accurate to avoid delays.

Your insurer has 60 days to approve or deny your claim. If denied, they must explain why in writing. You can appeal the decision or file a complaint with the Florida Department of Financial Services.

Common Mistakes That Get Florida PIP Claims Denied

Missing the 14-day treatment window is the top reason for denials. Even if you think you’re fine, get checked out. Some injuries, like whiplash, can take days to surface.

Another common pitfall is using an unapproved provider for your initial treatment. Chiropractors and massage therapists don’t count for the first visit. You need a medical doctor, osteopath, or dentist to start the clock.

Incomplete or inaccurate paperwork can also derail your claim. Make sure your medical provider uses the correct Florida PIP billing forms and includes all necessary details. Errors or omissions can lead to automatic denials.

Finally, waiting too long to file can be a problem. While Florida doesn’t have a strict deadline for submitting claims, delays can raise red flags with insurers. File as soon as possible after receiving treatment.

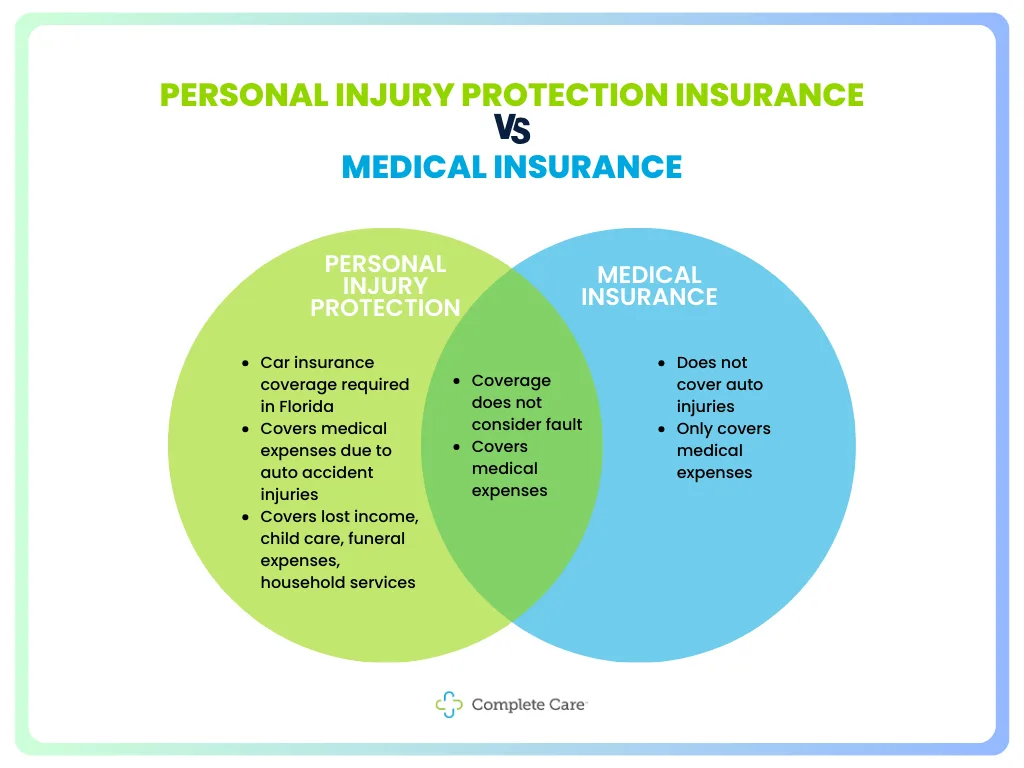

PIP vs. Health Insurance vs. MedPay: Which Pays First?

PIP is always primary for car accident injuries in Florida. Your health insurance only kicks in after PIP’s $10,000 limit is exhausted.

Image source: Bing (Web (fair-use with source credit))

MedPay is different. It’s optional coverage that pays medical expenses regardless of fault. Unlike PIP, it has no deductibles or co-pays and can cover costs like dental work or funeral expenses.

Here’s how they stack up:

| Coverage Type | Primary/Secondary | Deductible | Co-pay | Fault Required |

|---|---|---|---|---|

| PIP | Primary | Yes | 20% | No |

| Health Insurance | Secondary | Varies | Varies | No |

| MedPay | Primary or Secondary | No | No | No |

When You Can Sue After a Car Accident in Florida

Florida’s no-fault system limits lawsuits for minor injuries. You can only sue the at-fault driver if your injuries meet the state’s "serious injury" threshold.

This includes permanent injuries, significant scarring, or disfigurement. Death also qualifies for a lawsuit. For everything else, PIP is your only option for medical expenses.

If your case meets the threshold, you can pursue compensation for pain and suffering, lost wages beyond PIP’s limits, and future medical costs. But proving a serious injury often requires extensive medical documentation.

Florida PIP Costs: What You’ll Pay and How to Save

Florida’s minimum PIP requirement is $10,000, but your premium depends on several factors. Your driving record, age, location, and vehicle type all play a role. Urban areas like Miami or Orlando typically have higher rates due to increased accident risks.

You can lower your premium by choosing a higher deductible. A $1,000 deductible will reduce your monthly cost, but you’ll pay more out of pocket after an accident. Weigh the savings against the risk.

Other ways to save include bundling your auto insurance with homeowners or renters insurance. Many insurers offer discounts for safe driving records or completing defensive driving courses.

Expert Tips to Maximize Your PIP Medical Coverage

Always seek medical attention immediately after an accident, even if you feel fine. Some injuries, like internal bleeding or concussions, may not be obvious right away. The 14-day rule is strict, and missing it voids your PIP benefits.

Keep detailed records of all medical treatments, expenses, and communications with your insurer. This includes doctor’s notes, receipts, and any correspondence. Documentation is key to ensuring your claim is processed smoothly.

If your insurer denies your claim, don’t accept it without question. Request a written explanation and review it carefully. You have the right to appeal the decision or file a complaint with the Florida Department of Financial Services.

Frequently Asked Questions

Does Florida PIP cover chiropractic care?

Yes, but only if a medical doctor refers you. Initial treatment must come from a licensed MD, osteopath, or dentist. Chiropractors can provide follow-up care if your injury is classified as an Emergency Medical Condition.

What happens if my medical bills exceed my PIP limit?

Your health insurance can cover the remaining 20% of medical costs after PIP pays its share. If you have MedPay, it can also help with additional expenses. Without these, you’ll be responsible for the balance.

Can I use PIP to cover lost wages?

Yes, PIP covers 60% of your lost wages if you can’t work due to accident-related injuries. This is subject to your policy’s $10,000 limit, which also includes medical expenses.

How long do I have to file a PIP claim in Florida?

While there’s no strict deadline, you should file as soon as possible. Your insurer has 60 days to approve or deny your claim once submitted. Delays can raise red flags and complicate the process.

Does PIP cover passengers in my car?

Yes, PIP extends to passengers in your vehicle, as well as family members driving your car. It also covers you as a pedestrian or cyclist if you’re hit by a vehicle.