Florida’s $10,000 personal injury protection PIP insurance requirements are non-negotiable if you own a car in the state. This no-fault coverage kicks in after an accident, paying your medical bills and lost wages regardless of who caused the crash. As of 2026, it’s one of the few mandatory auto insurance rules in Florida.

The law requires every driver to carry at least $10,000 in PIP, plus $10,000 in property damage liability. Miss this, and you risk fines, license suspension, or even vehicle impoundment.

Image source: Bing (Web (fair-use with source credit))

Quick Answer

Florida requires $10,000 in PIP coverage for all vehicle owners. It covers 80% of medical bills and 60% of lost wages after an accident. You must seek treatment within 14 days to qualify.

This is separate from property damage liability.

Why Florida Forces You to Carry PIP (And What Happens If You Don’t)

Florida’s no-fault system means your own insurance pays your injuries first, no matter who caused the crash. The goal is to reduce lawsuits and speed up claims. Without PIP, you can’t legally register or drive your car in the state.

Penalties for driving without PIP start with a license and registration suspension. Reinstatement fees range from $150 to $500. Repeat offenses can lead to higher fines or even vehicle impoundment.

How Florida’s No-Fault PIP System Actually Works

After an accident, your PIP coverage pays your medical expenses up to $10,000, regardless of fault. It also covers 60% of lost wages if you can’t work. This system is designed to get you treatment fast without waiting for fault determinations.

The trade-off is that you can’t sue the other driver for minor injuries. PIP is your primary coverage, and health insurance may cover gaps. Florida’s system prioritizes quick payouts over lengthy legal battles.

Image source: Bing (Web (fair-use with source credit))

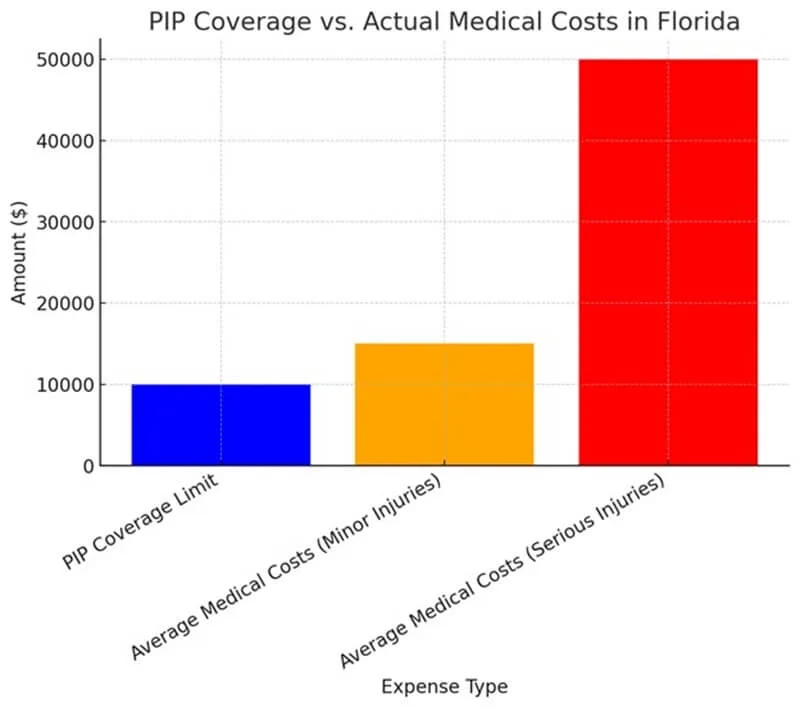

What Your $10,000 PIP Policy Covers (And What It Doesn’t)

Your PIP policy covers 80% of reasonable medical expenses related to the accident. This includes hospital bills, doctor visits, and rehabilitation. It also pays 60% of lost wages if you’re unable to work.

What it doesn’t cover includes property damage, pain and suffering, or non-emergency treatments after 14 days. PIP also excludes injuries sustained while committing a felony or driving under the influence.

| Covered | Not Covered |

|---|---|

| Medical bills (80%) | Property damage |

| Lost wages (60%) | Pain and suffering |

| Death benefit ($5,000) | Non-emergency late treatment |

The 14-Day Rule: How One Missed Deadline Can Cost You Everything

Florida’s PIP law requires you to seek medical treatment within 14 days of the accident. If you miss this window, you forfeit your right to PIP benefits. Even a single day late can mean no coverage for your injuries.

The clock starts the day of the accident, not when you first feel pain. Emergency room visits, urgent care, or a doctor’s appointment all count. Without timely treatment, your insurer can legally deny your claim.

PIP Deductibles in Florida: $0 vs. $250 vs. $500 vs. $1,000

Your deductible is what you pay out of pocket before PIP kicks in. A $0 deductible means full coverage starts immediately. Higher deductibles lower your premium but increase your upfront costs after a crash.

The most common choices are $250, $500, or $1,000. A $1,000 deductible can reduce your annual premium by 10-20%. But if you can’t afford the deductible after an accident, you’ll struggle to access benefits.

Who’s Covered Under Your PIP Policy (And Who Isn’t)

Your PIP covers you, your passengers, and even pedestrians or cyclists hit by your car. It also extends to your children if they’re injured in a school bus accident. Family members driving your car are typically covered too.

It doesn’t cover motorcyclists, out-of-state drivers without Florida PIP, or injuries from non-vehicle incidents. PIP also excludes intentional injuries or those sustained while committing a crime.

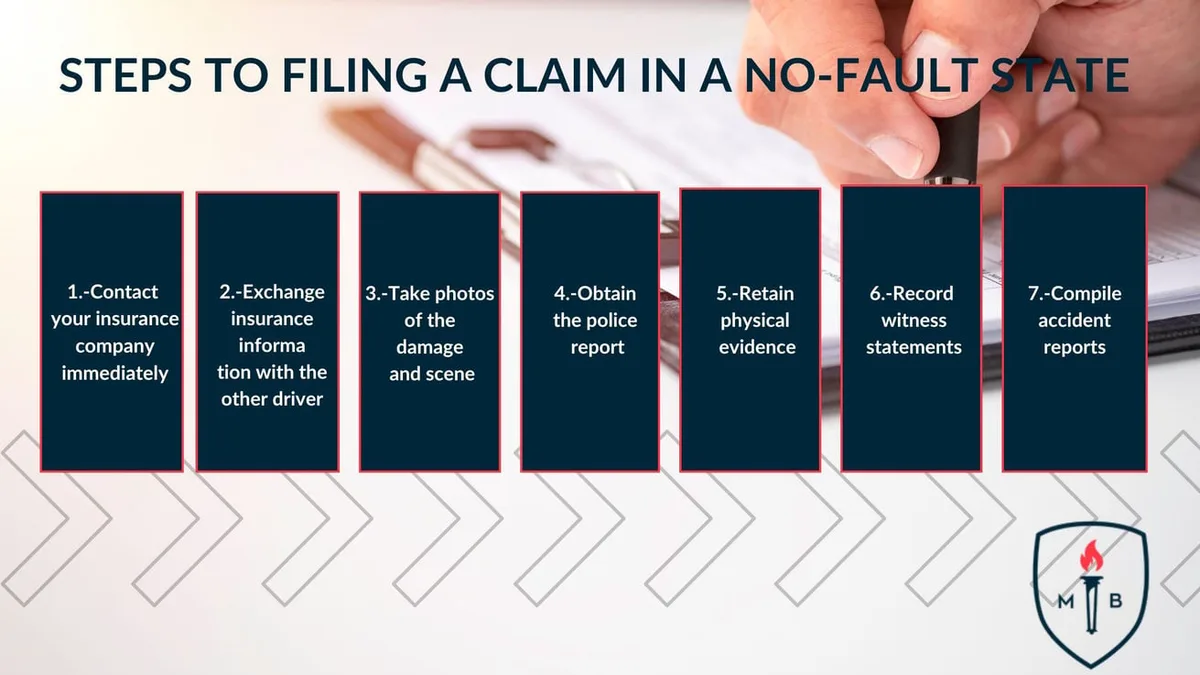

Step-by-Step: How to File a PIP Claim in Florida

First, seek medical attention within 14 days of the accident. Then notify your insurer immediately, even if you weren’t at fault. Provide your policy number, accident details, and any police report information.

Submit all medical bills and lost wage documentation to your insurer. They’ll review and process your claim, usually within 30 days. Keep copies of everything for your records.

Image source: Bing (Web (fair-use with source credit))

Florida PIP vs. Bodily Injury Liability vs. Health Insurance

PIP covers your injuries regardless of fault and pays quickly. Bodily Injury Liability (BIL) covers others’ injuries if you’re at fault but isn’t required for all drivers. Health insurance may cover gaps but often has higher out-of-pocket costs.

PIP is mandatory in Florida, while BIL and health insurance are optional. PIP also covers lost wages, which health insurance doesn’t. BIL is only for others, not you or your passengers.

Common PIP Mistakes That Get Claims Denied

Waiting more than 14 days to see a doctor is the top reason for denied claims. Missing documentation or submitting incomplete medical records can also lead to rejection. Not reporting the accident to your insurer immediately is another common pitfall.

Using PIP for non-emergency treatments after the 14-day window will result in denial. Fraudulent claims, like exaggerating injuries, can lead to legal consequences. Always follow the exact process outlined in your policy.

How Much PIP Costs in Florida (And How to Lower Your Premium)

Florida’s average PIP premium ranges from $1,200 to $2,500 per year. Your exact cost depends on your driving record, vehicle type, and location. Urban areas like Miami and Tampa tend to have higher rates due to increased accident risks.

You can lower your premium by choosing a higher deductible or bundling with other policies. Safe driving discounts and maintaining continuous coverage also help. Always compare quotes from multiple insurers to find the best rate.

Image source: Bing (Web (fair-use with source credit))

Florida PIP Fraud: Red Flags and How to Protect Yourself

PIP fraud is a serious issue in Florida, often involving staged accidents or inflated medical bills. Be wary of strangers waving you into traffic or sudden stops by unknown drivers. These are common tactics used to create fraudulent claims.

Always document the scene with photos and gather witness information. Report suspicious activity to your insurer and the Florida Division of Insurance Fraud. Never sign blank medical forms or agree to unnecessary treatments.

What to Do If You’re in an Accident (PIP Checklist)

First, call 911 if there are injuries or significant damage. Exchange information with the other driver, including insurance details and contact info. Take photos of the scene, vehicle damage, and any visible injuries.

Seek medical attention immediately, even if you feel fine. Some injuries take time to appear. Notify your insurer as soon as possible to start the claims process.

Frequently Asked Questions

Does PIP cover me if I’m at fault for the accident?

Yes. PIP is no-fault coverage, so it pays your medical bills and lost wages regardless of who caused the crash.

Can I use PIP for non-car-related injuries?

No. PIP only covers injuries sustained in a vehicle accident. It doesn’t apply to other types of incidents.

What happens if my medical bills exceed $10,000?

Your PIP will pay up to its $10,000 limit. After that, you may need to use health insurance or other coverage for remaining costs.

Do I need PIP if I don’t own a car but drive occasionally?

Yes. If you drive any vehicle in Florida, you must have PIP coverage. This includes borrowed or rented cars.

Can I opt out of PIP if I have health insurance?

No. Florida law requires PIP for all vehicle owners, regardless of other insurance coverage.

How long do I have to file a PIP claim?

You must seek medical treatment within 14 days of the accident to qualify for PIP benefits. Claims should be filed with your insurer as soon as possible.