Connecticut mandatory liability insurance minimum coverage limits and verification exist to keep drivers legally protected on the road. If you're registering a car or just want to avoid fines, knowing the exact requirements is non-negotiable.

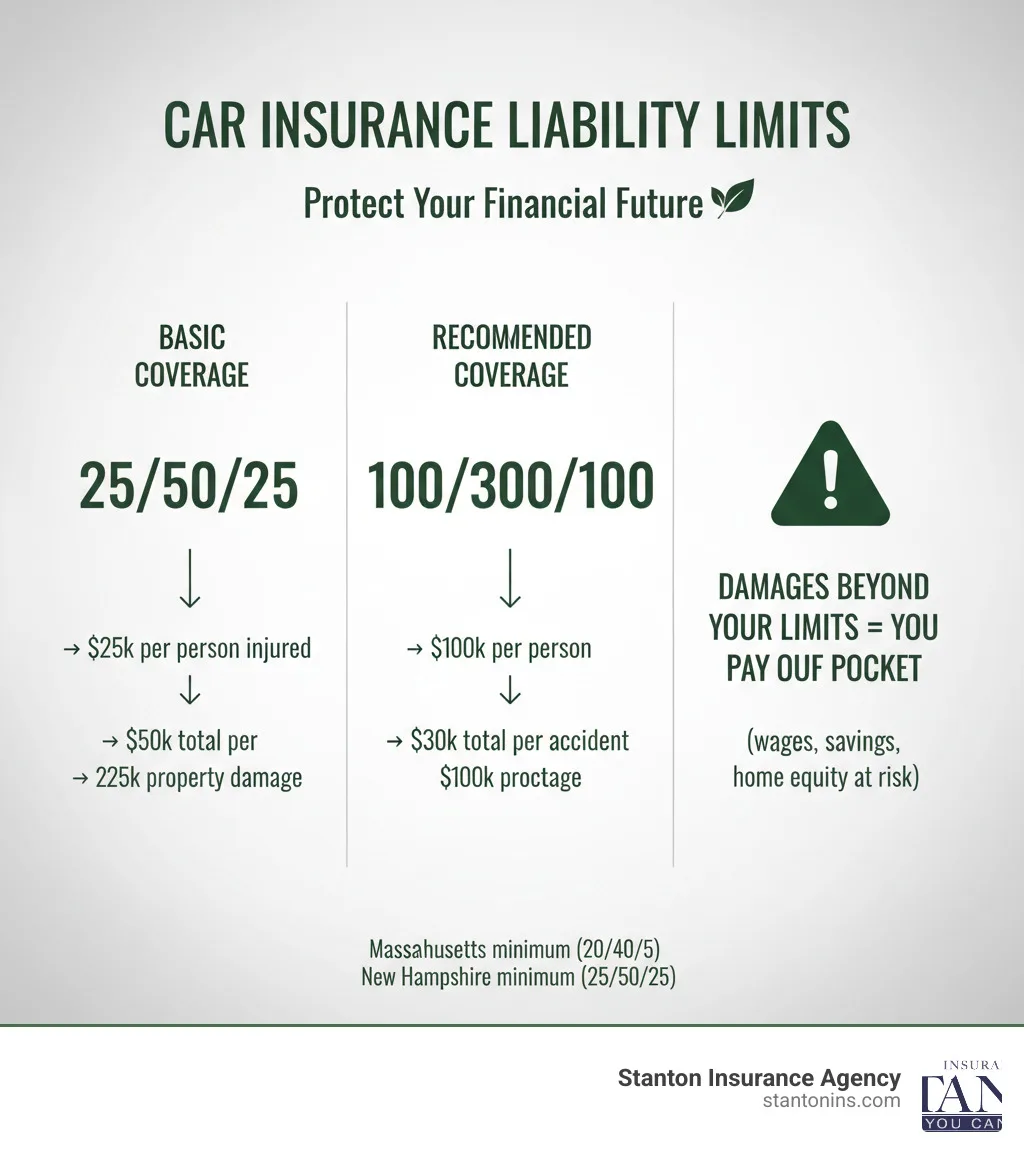

As of 2026, Connecticut requires at least 25/50/25 coverage. That means $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. Here's what that actually means for you.

Image source: Bing (Web (fair-use with source credit))

Quick Answer

Connecticut mandatory liability insurance minimum coverage limits and verification require 25/50/25. That's $25,000 bodily injury per person. $50,000 bodily injury per accident. $25,000 property damage per accident. Uninsured motorist coverage is also mandatory.

Image source: Bing (Web (fair-use with source credit))

CT's Minimum Coverage Limits

Connecticut's minimum liability insurance breaks down into three numbers: 25/50/25. The first two cover bodily injury. The last one covers property damage.

Here's what each part covers in real terms:

| Coverage Type | Limit | What It Covers |

|---|---|---|

| Bodily Injury (per person) | $25,000 | Medical bills for one person injured in an accident you cause |

| Bodily Injury (per accident) | $50,000 | Total medical coverage for all injuries in a single accident |

| Property Damage (per accident) | $25,000 | Damage to another person's car, fence, building, or other property |

These are the absolute minimums. If damages exceed these limits, you're personally responsible for the difference. A single hospital visit can easily blow past $25,000.

How Connecticut's Insurance Requirements Work

Connecticut's financial responsibility law requires every registered vehicle to carry liability insurance. The state doesn't just take your word for it. It checks electronically.

The Connecticut Insurance Department oversees these rules. Your insurer must report active policies to the state's verification system. If your coverage lapses, the DMV gets an alert automatically.

This system confirms every driver on the road meets the minimum requirements. It also means you can't fake insurance. Your policy status is checked in real time.

What's Covered (and What's Not) Under CT's Minimums

The 25/50/25 limits cover damages you cause to others. They do not cover your own injuries or vehicle damage.

| Coverage Type | What It Covers | What It Doesn't Cover |

|---|---|---|

| Bodily Injury Liability | Others' medical bills from an accident you cause | Your own medical bills or passengers' injuries |

| Property Damage Liability | Damage to others' property | Damage to your own car |

| Uninsured Motorist Coverage | Your injuries if hit by an uninsured driver | Damage to your car (unless you add property damage coverage) |

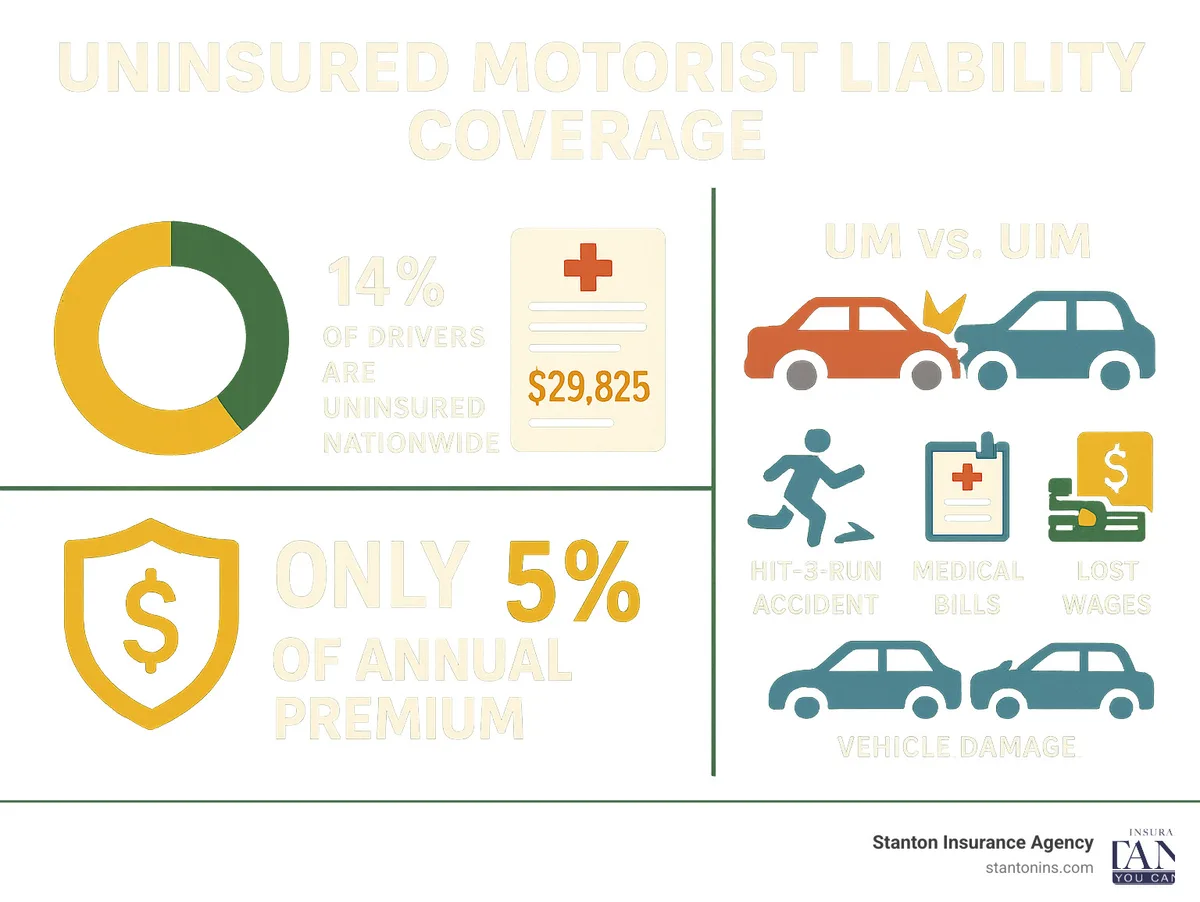

Connecticut requires uninsured motorist bodily injury coverage. This kicks in when the at-fault driver has no insurance or not enough to cover your damages.

Why Uninsured Motorist Coverage Is Non-Negotiable in CT

Connecticut mandates uninsured motorist coverage because roughly 1 in 8 drivers nationwide are uninsured, according to the Insurance Information Institute. Without this coverage, you could pay your own medical bills after an accident that wasn't your fault.

The minimum uninsured motorist limits in CT match the bodily injury liability limits: $25,000 per person and $50,000 per accident. This is separate from your liability insurance.

Image source: Bing (Web (fair-use with source credit))

This protection keeps you from being financially ruined by someone else's irresponsibility. It adds a small amount to your premium but provides a major safety net.

How Connecticut Verifies Your Insurance

Connecticut uses an electronic verification system to check insurance status in real time. Your insurance carrier reports active policies directly into the DMV database.

If your coverage lapses, the DMV sends you a notice by mail. You have a short window to provide proof of new insurance or you'll face penalties.

Image source: Bing (Web (fair-use with source credit))

Driving without valid insurance can result in fines starting at $200. Repeat offenses or failure to reinstate coverage can lead to registration suspension. If your license gets suspended, the process to get it back can be complex, much like the strict license suspension rules we see in other states.

Step-by-Step: Proving Insurance in CT

You must carry proof of insurance whenever you drive. Digital copies on your phone are accepted as long as they're legible.

If a police officer stops you, present your insurance card immediately. The officer will verify it against the state database on the spot.

For DMV transactions like registration renewal or getting a Real ID, you'll need to show proof. The system cross-checks your policy status automatically. Knowing the specific documentation requirements can save you a trip back to the DMV.

The Real Cost of Skipping or Faking Insurance in Connecticut

Driving uninsured in CT carries serious penalties. A first offense costs between $200 and $500 in fines.

Your registration can be suspended until you provide proof of insurance. Reinstatement fees add to the financial hit.

Faking insurance documents is a criminal offense. It can lead to higher fines, license suspension, or even jail time in severe cases.

Common Mistakes That Get CT Drivers in Trouble

Letting your policy lapse. Even a one-day gap can trigger a DMV alert. Set up automatic payments to avoid accidental lapses.

Assuming your out-of-state policy works. Always confirm your coverage meets or exceeds the 25/50/25 limits. Some states have lower minimums.

Forgetting to update your address. Your insurer needs your current address on file for verification to work properly. Keeping your address current with the DMV is just as important as maintaining your coverage.

Only carrying a paper card. Digital proof is fine, but make sure you can access it quickly. A screenshot in your photos works better than hunting through emails.

When You Might Need More Than the Minimum

The state minimums may not cover everything in a serious accident. Medical bills and property damage can quickly exceed 25/50/25.

If you own a home or have significant assets, higher limits protect you from lawsuits. Consider an umbrella policy for extra liability coverage.

Leased or financed vehicles often require full coverage. Check your contract for specific insurance requirements. If you're on a tight budget, you might look into low-cost auto insurance options as a starting point.

How to Check Your Own Insurance Status in CT

You can verify your coverage through the Connecticut DMV's online portal. Enter your license plate or VIN to see if your policy is active in the system.

If you spot a lapse, contact your insurer immediately. They can update the state database once you reinstate coverage.

For extra peace of mind, request a current insurance card from your provider. It serves as backup proof if the electronic system has a delay.

Frequently Asked Questions

What happens if I'm caught driving without insurance in CT?

You'll face a fine between $200 and $500 for a first offense. Your registration may also be suspended until you provide proof of insurance.

Does Connecticut require full coverage?

No, Connecticut only mandates liability and uninsured motorist coverage. Full coverage is optional unless your lender or lessor requires it.

Can I use digital proof of insurance in CT?

Yes, Connecticut accepts digital insurance cards on your phone. Just make sure the document is clear and easy to read.

How often does CT check insurance status?

The DMV verifies insurance electronically in real time. Your insurer reports coverage status directly to the state database.

Do I need uninsured motorist coverage in CT?

Yes, Connecticut requires uninsured motorist bodily injury coverage. The minimum limits match your liability coverage at 25/50.

Final Checklist: Are You Legally Covered in CT?

- Confirm your policy meets the 25/50/25 liability minimums.

- Check that uninsured motorist coverage is included in your policy.

- Carry proof of insurance at all times, digital or paper.

- Verify your coverage is active in the DMV's system.

- Update your insurer if you move or change vehicles.

- Set reminders for policy renewals to avoid lapses.